Is Canada losing the exploration game?The hurdles to increased exploration spending in Canada

Canada’s status as the hands-down favourite destination for exploration investment is eroding as mineral deposits become more difficult to access, competition for capital broadens, and regulatory uncertainty continues to irk potential investors.

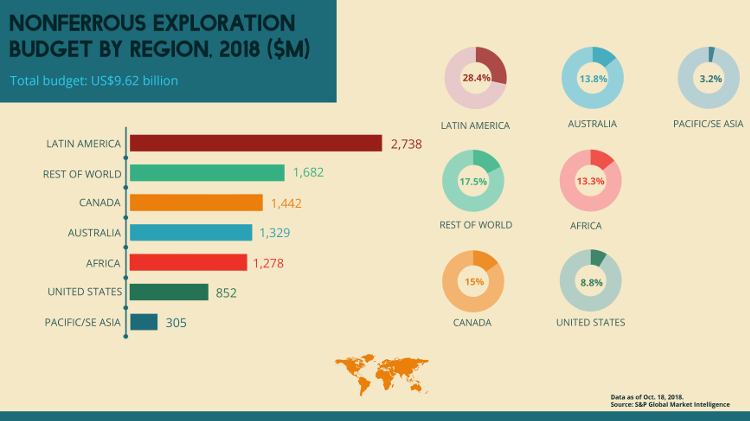

Over the past decade, Canada’s share of global exploration spending for non-ferrous minerals slipped from 20.5 per cent in 2008 to less than 14 per cent in 2017 before inching back to 15 per cent in 2018, according to S&P Global Market Intelligence, which bases its analysis on private sector spending intentions. Although Canada remains a narrow favourite among individual countries, S&P treats it as a region “for the purpose of continental-scale comparisons.” As such, it has dropped to third place behind Latin America and the “Rest of the World” (mostly Europe and Asia) from second place in 2008.

There is a lot at stake for the country. The mineral exploration and mining industry employs nearly 630,000 in Canada and directly and indirectly contributes more than three per cent to the country’s gross domestic product. Mineral exports account for about 19 per cent of Canada’s total domestic exports, while Toronto’s TSX and TSX-V capture 51 per cent of all global mining financing transactions. The country is a world leader in legal, engineering, geological, equipment and financial expertise.

In order to maintain this exceptional status, Canada must continue to attract explorers willing to risk capital to find the next generation of mineral deposits. Providing better access to the far north, ensuring regulatory certainty, and supporting research and innovation may be the most obvious means to that end, according to industry watchers.

The explanation for Canada’s shrinking piece of the exploration spending pie is complicated, said Glenn Mullan, president of PDAC, the advocate for Canada’s mineral exploration and development community. But there are a few factors that stand out.

Lack of infrastructure means that otherwise robust and well-delineated deposits in the north have been effectively stranded while many more remain unexplored. Competition, including from dozens of African countries that view investment in the mineral sector as key to prosperity, is spreading available capital thin. And regulatory uncertainty adds an extra layer of chance to the already risky business of mineral exploration.

The mining industry can, however, count a recent win on the regulatory front. The government of Canada in late November committed to a five-year renewal of the Mineral Exploration Tax Credit (METC), designed to help companies raise equity funds for exploration in Canada. Every year, PDAC has lobbied the federal government to renew the METC for a minimum of three years without knowing if, or for how long, the credit will be renewed. The government introduced the 15 per cent tax credit in 2000 and has consistently offered single year renewals.

“We are pleased that the government has heard our concerns about Canada’s waning competitiveness and adopted our recommendation,” said Lisa McDonald, PDAC’s interim executive director and COO, in a press release. “Renewal of the METC for five years will help to provide greater certainty and boost confidence for investors, and signals government’s appreciation of the importance of our junior exploration sector.”

The decline in exploration market share, which still leaves Canada in a leading position with about 15 per cent of global spending, is less dramatic when you take into account government spending estimates (rather than company budgets) and bulk mineral exploration, said Richard Schodde of MinEx Consulting in Australia.

But he said he agrees that Canada’s juniors – a large driver of exploration spending in the country – have struggled to raise capital of late. “A big feature of Canada’s exploration scene is its very large pool of junior explorers, much bigger than many other jurisdictions around the world. Their ability to raise money is highly sensitive to the overall economic business cycle – and commodity prices in particular. It’s great on the way up, but it’s tough on the way down.”

According to S&P, there are 1,651 companies in the world actively exploring – which is down by a third from 2012 levels, when global exploration spending peaked – while gold has lost about 25 per cent of its value. Copper averaged at US$3.61 per pound in 2012 but was trading below US$3 in 2018.

Geopolitical factors beyond Canada’s control may also be restricting investment, said Schodde. U.S. President Trump’s trade sanction rhetoric has put an added damper on metal prices this year.

Include China in the equation and it becomes clear that not only Canada but other established mining jurisdictions are falling behind in the competition for capital. According to Schodde, China spent more on domestic exploration in 2013 than Australia and Canada combined. Because exploration in China is mostly carried out by the state, S&P’s analysis tends to under-report what is happening there.

Some Canadian provinces and territories are faring better than others. Saskatchewan, Ontario, and Quebec still rank among the top 10 most attractive jurisdictions in the world, according to the Fraser Institute’s 2017 survey of mining companies, an attempt to assess how mineral endowments and public policy factors affect exploration investment. Newfoundland and Labrador takes the 11th spot out of 91 jurisdictions included in the survey.

Quebec, in particular, has made substantial efforts to keep explorers satisfied. For example, the province is spending about $1.3 billion on infrastructure and other projects by 2020 in the hopes of attracting $22 billion in private-sector investment in the north, including from mineral explorers and developers. It is working.

“Quebec is open for business when it comes to exploration,” said Tony Makuch, President and CEO of Kirkland Lake Gold, which owns shares in several junior mining companies active in the Abitibi gold belt of northwestern Quebec, such as Osisko Mining, Metanor Resources, and Bonterra Resources. “There is a lot more clarity around responsibilities towards local communities and better incentives than in other provinces.”

On the other hand, Makuch is increasingly frustrated with exploration in Ontario, where Kirkland Lake operates the Macassa, Holt and Taylor gold mines. He said changes to Ontario’s Mining Act and lack of clarity around how to forge agreements with Indigenous communities is driving explorers out of the province.

“Look at the Ring of Fire [an expansive metal-rich area in the James Bay Lowlands of Ontario discovered a decade ago that is stranded by both lack of infrastructure and politics] – is it getting explored? Is it getting developed? We need clearer rules and a better idea of what communities want.”

Other provinces are also losing their appeal as attractive places to invest exploration dollars. Alberta has slipped from 4th place to 49th place, Manitoba from 8th to 18th place, and New Brunswick from 6th to 30th place in the Fraser Institute survey over the past decade. Despite attractive geology, British Columbia has been shut out of the top 10 jurisdictions for years because of regulatory uncertainty and concerns regarding disputed land claims.

Agnico Eagle Mines and Hudbay Minerals – both of which once spent most of their multi-million dollar exploration budgets in Canada, but have spread spending among several countries in recent years – either did not respond to queries (Agnico) or declined to comment (HudBay) for this story.

But Agnico Eagle CEO Sean Boyd put in a plug for Nunavut, ranked 26th in the Fraser Institute survey, at The Northern Miner’s Progressive Mines Forum in October. “Nunavut is one of those rare places from a mining perspective – it has great mineral potential and you can actually get things done,” said Boyd, whose company has pledged $5 million to build a university in the territory where it operates the Meadowbank gold mine and is developing the nearby Meliadine project for start-up next year. “As Canadians, we should be championing places like Nunavut because it is going to be a huge value generator for this country for some time.”

As for Kirkland Lake Gold, it will spend the bulk of its $75-90 million exploration budget in Australia this year, where the company owns the Fosterville and Cosmo gold mines. The spending shift to Australia is not an intentional snub of Canada, said Makuch, but more related to the stage of the company’s projects (Macassa is moving from surface to underground exploration) and the natural end to a $16-million exploration push in Canada financed by flow-through funding raised in 2016.

But he said Canada could benefit from Australia’s clearer rules around community engagement and its ability to sustain investor interest in exploration. “Canada is not as friendly toward new discoveries as people tend to think. In Australia, the rules are better defined and there is support for exploration. The investment community is willing to put money into resources and take a long-term approach.”

Alarmed by the declining competitiveness of Canada’s mineral industry, PDAC and other members of the Canadian Mineral Industry Federation (CMIF) presented a brief to the 75th Energy and Mines Ministers’ conference in Iqaluit in August suggesting reasons for the decline and proposing some solutions. The following factors are particularly relevant to exploration.

Far north infrastructure

Deposits are being abandoned, or remaining unexplored, in the north because it is difficult and expensive to access them. As accessible mineral deposits in historic camps such as Val d’Or, Kirkland Lake and Flin Flon are mined out, exploration must logically move farther north. But lack of infrastructure makes development uneconomic.

“PDAC’s 2016 report, ‘Unlocking Northern Resource Potential: The Role of Infrastructure,’ showed there are around 146 undeveloped projects in the three territories, or over 75 per cent of identified significant deposits that are pretty much stranded or orphaned. They have been well explored and delineated and some even have feasibility studies, but infrastructure is the main impediment for advancing them to development,” said Mullan.

The Canadian government has taken steps to address the shortfall through programs such as a bilateral agreement with Nunavut that will provide more than $566 million over the next decade to infrastructure projects in the territory. Another initiative called the National Trade Corridors Fund will dedicate up to $400 million for transportation initiatives in the Yukon, Northwest Territories and Nunavut. Transport Canada is calling for proposals for more roads, airports, ports and bridges through the program.

Still, Canada lags well behind Europe and Asia in developing its northern regions. “We only need to look at other Nordic countries to see what comparable regions are doing with infrastructure,” said Mullan. “We need to up our game in terms of northern access. There is a general recognition that there is a gap there we should be addressing.”

Regulatory uncertainty

The CMIF brief highlights specifics such as the way mining projects are treated under the Canadian Environmental Assessment Act, 2012 (currently under revision), but the CMIF’s overriding concern is that uncertainty around the review and implementation of policy and legislation at both the federal and provincial levels is discouraging investment.

The federation urged mines ministers to ensure that Canada’s regulatory regimes are “effective, efficient, predictable and balanced” in order to bolster Canada’s reputation as a safe place to invest. Streamlining provincial and federal regulations, for instance, would provide clarity and efficiency.

“Some other jurisdictions, such as Australia, have done a better job than us in coordinating their national, state and municipal governments,” said Mullan. “In Canada, we still have a lot of room for improvement.”

The Crown’s duty to consult and accommodate Indigenous groups on mineral projects is exacerbating the uncertainty because there is such a patchwork of policies depending on the jurisdiction. The CMIF said it would like to see governments increase their social investment in Indigenous communities, such as for housing and water, implement government resource revenue sharing with communities, and address some of the challenges that have arisen as a result of the duty to consult.

Competition

Jurisdictions around the world are recognizing the value of early stage exploration and devising new ways to attract investors. Botswana, for example, recently launched an online geoscience data portal that allows anyone to search for all the available geoscience data within a selected geographic area.

Australia, Canada’s main competitor with a 13.8 per cent share of non-ferrous exploration spending in 2018, according to S&P, has increased its incentives for grassroots exploration. A new tax incentive scheme introduced this year allows greenfield exploration programs to distribute tax losses as a credit to Australian resident shareholders. And a few states offer up to a 50 per cent refund for innovative exploration drilling projects.

Land withdrawal and geoscience funding

Land use legislation – such as Ontario’s Far North Act, which will protect a large area of provincial land in the north from development – often fails to consider mineral potential. PDAC is advocating for a more balanced approach to land withdrawal that incorporates geoscience and mineral resource assessment into land management decisions.

“No one disputes that there are areas that need to be protected, but geoscience should always be part of that decision-making process,” said Mullan.

Canada used to be a world leader in funding geoscience research, such as geological mapping in underexplored areas, but its standing has dropped considerably over the past decade. The CMIF brief calls for increased funding for the Geological Survey of Canada, particularly for work in the far north, and incentives for testing new exploration technologies and techniques.

Once again, Australia is leading. The country recently launched a $218 million research organization (MinEx CRC) to develop mineral discovery technologies for hidden deposits and boost drilling productivity with simultaneous data collection. The CRC is also launching a National Drilling Initiative (NDI), the first collaboration of government geological surveys, researchers and industry in the world to drill for mineral deposits in under-explored areas.

The metrics for Canada are not all gloomy, however. The latest numbers from S&P suggest that budgets earmarked for Canada may be on the rise again, increasing by 31 per cent to US$1.44 billion in 2018. And when companies do choose to explore here, they can expect a decent bang for their buck. Schodde’s research shows that the return on investment for exploration in Canada is as good, if not better, than in Australia or the United States, who are Canada’s two main competitors for exploration spending.

“My personal view is that the federal and provincial governments do a good job of supporting the industry through tax incentives and a strong R&D base,” said Schodde. “Notwithstanding this, Canada still has some inherent challenges – namely the lack of infrastructure in the far north coupled with the challenges of exploring under progressively deeper cover in the more established districts in the south.”

If governments at both levels were to adopt even some of the CMIF’s suggestions to the mines ministers this year, such as building northern infrastructure, investing in geological and drilling research and improving regulatory certainty, Canada could regain its global reputation as the strong favourite for exploration investment and secure a brighter future for the domestic industry as a whole.

More Projects

Quebec’s golden pockets

Exploration is stagnant around most of the world, but Quebec’s gold camps in the Abitibi and James Bay regions offer a ray of light in an otherwise dark tunnel

Hope for the future

TMAC’s high-grade Hope Bay gold project in the Kitikmeot region of Nunavut is nearing start up